Closing of Investigation No VIZSG/028/2024 – Projects in Acsa

Cikk publikálásának ideje:

The Integrity Authority (“Authority”) conducted an ex officio investigation into two projects of the Municipality of Acsa, supported under the Territorial and Settlement Development Operational Programme (TOP Plus). The projects subject to investigation received a total of HUF 583,351,376 in funding. One project included the construction of a new small-scale day nursery with a capacity of eight children, while the other one carried out the redevelopment and energy efficiency modernisation of buildings that house service accommodations and doctors’ surgeries.

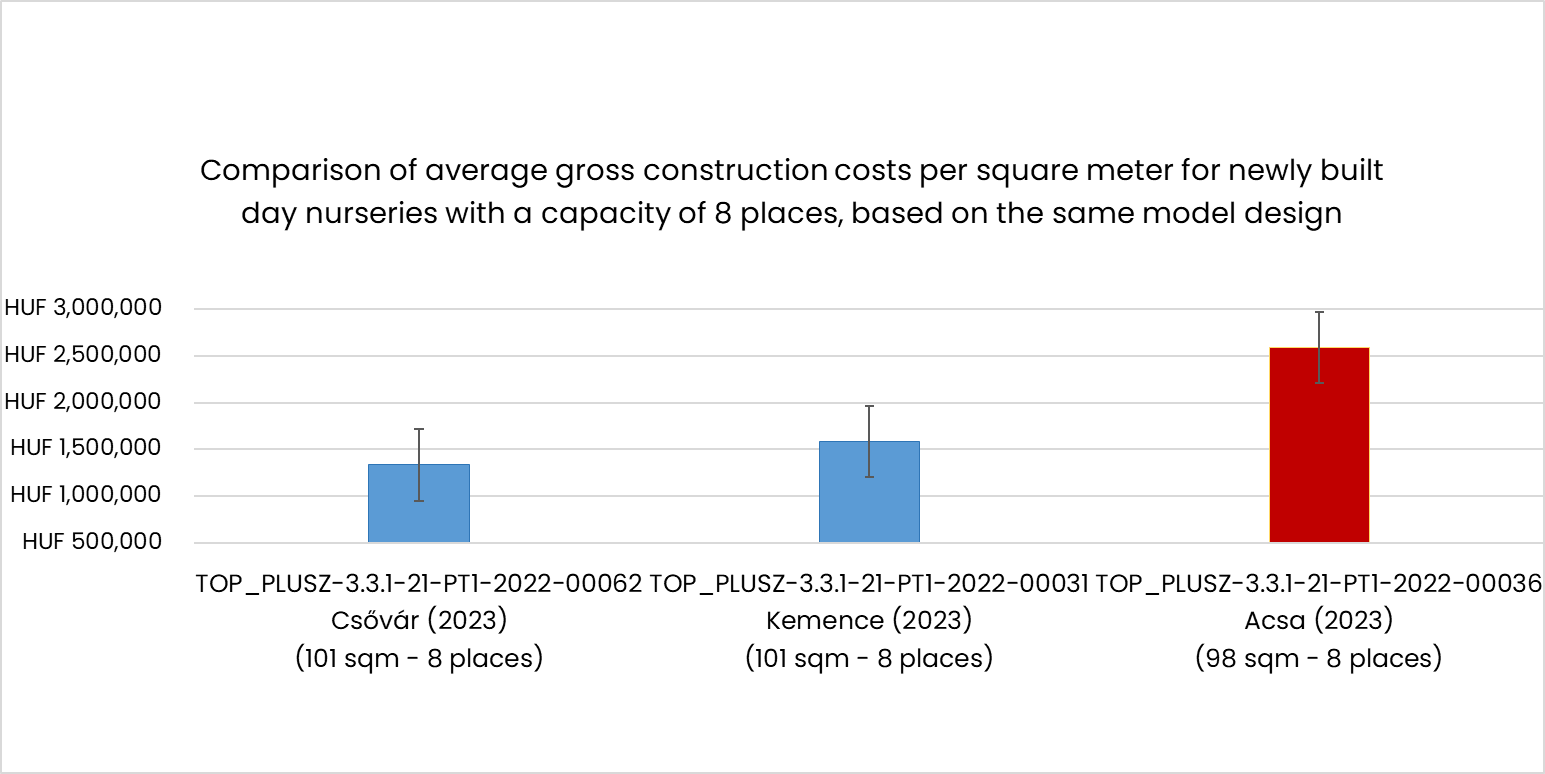

The Authority’s comparative analysis found that the construction costs of the mini day nursery in Acsa likely exceeded the arm’s length price at the time of construction by HUF 109,906,787 gross – or 77% – with a construction cost of nearly HUF 2.6 million gross per square meter. The Authority based this conclusion on the fact that in the same period and under the same funding scheme, two additional mini nurseries were also constructed based on the same designer’s model designs – which, in the case of facilities with a capacity of eight places, are almost identical – and had an average construction cost of only HUF 1.5 million gross per square meter, as illustrated in the following figure.

Overpricing may have occurred because the contracting authority failed to comply with the requirements of the efficient and responsible use of public funds during the public procurement procedure. On the one hand, the designer cost estimate supporting the estimated value may have been falsified; and on the other hand, during the public procurement procedure for the new mini day nursery, the contracting authority invalidated the tenders of seven of the ten economic operators, even though their tenders were substantially more favourable compared to that of the successful tenderer.

As for the other project, which involved the renovation of doctors’ surgeries and service accommodations, the same company once again emerged as winner in the public procurement procedure. Furthermore, the independent accredited public procurement expert was the same person as well. Suspicions arose in this project as well that the contracting authority unjustifiably increased the estimated value of the public procurement procedure, as it had been determined based on two indicative price quotations selected by the contracting authority despite the availability of the statutory designer cost estimate, which indicated a total investment cost 37% lower. Two tenderers that participated in this public procurement procedure also took part in the procurement process of the other investigated project. Instead of conducting a public tender for what was essentially a construction project with more simple technical content, the contracting authority opted for a two-stage negotiated procedure; but in spite of this, it ultimately held no negotiations following the submission of the tenders, thereby unnecessarily precluding the possibility of more favourable tenders being submitted.

It was observed in both projects that the total amount of the contract concluded with the successful building contractor was almost identical to the originally awarded funding related to construction projects.

Furthermore, the Authority’s investigation identified a subcontractor that supposedly did not issue an invoice to the successful main contractor, thereby giving rise to a suspicion of non-compliance with invoicing obligations.

Based on suspicions of irregularities uncovered in connection with the conducted public procurement procedures, the Authority initiated proceedings with the Public Procurement Authority and the Public Procurement Arbitration Board, and proposed that the Managing Authority recover the funds affected by irregularities in both projects.

In addition, the Authority filed a criminal complaint against unknown person on suspicion of the use of a forged private document and budget fraud, and also notified the National Tax and Customs Administration over a suspected failure to comply with invoicing obligations.

The Authority issued forward-looking recommendations to both the Managing Authority and the Intermediate Body to review their control procedures and improve their effectiveness.